- December 19, 2024

- Posted by: adminlin

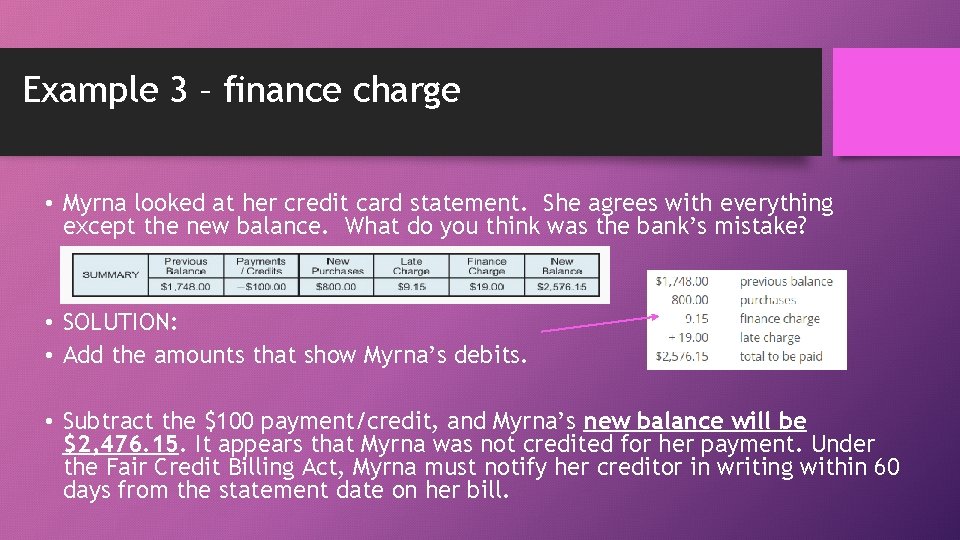

- Category: payday advance cash loans

You might be lured to pull out a new financial from the some section after paying it off, however, i have resisted one to tip and you can rather reserved this new currency we were paying for the borrowed funds inside the a bank account.

It means we don’t must set crisis costs on a good bank card, that is higher!

I personally like brand new comfort that have a paid back household gives me personally. Easily returned a life threatening car accident or sustained a great serious disease I’d not need to value losing my spot to real time. Is a question: If you had a paid household might you remove a home loan in it to set up the market? Hell No. Paying your house very early is not a math problem, it is coverage and you will freedom.

- Christine Luken

Discover a chance rates with obligations versus using the latest excessive dollars, however, debt often deal involved such as for example mental and personal baggage that we do not think you can always always think of it by doing this. i has actually eliminated financial obligation if you are paying to have an automobile from inside the dollars and you will aggressively settling student loans, and this compared to the market returns has actually ended up not to feel the optimal choice.

Certainly one of my loved ones members took out good 0% car loan, and that individuals carry out indicates to settle Today, whilst the loans is not charging things

I favor the fresh assurance of having my house reduced out-of. I dislike personal debt. Whenever i try a teenager, dad ideal I am able to spend my vehicle fix costs, whenever i visited the same store he performed. I recently didn’t exercise, since i have met with the currency and you may failed to handle having one hang more my direct. My spouce and i repaid each other the earliest house and you may our very own most recent domestic, of early. The initial one is an extremely low cost and try owner funded bank personal loans Louisiane therefore the proprietor told united states whenever we paid down it well very early, however take some from the dominant. Although not, toward the most recent household, I found myself functioning in the a leading stress business and you can planned to quit performing. I spent some time working aggressively towards repaying our house and not shortly after that I happened to be able to prevent working. We currently have a highly part-big date occupations working at home.

I think there clearly was discussion in this area because there are people that need certainly to beat the decision due to the fact often purely analytical or emotionally. However, as many over features commented, the new variables must decide is actually much messier. I’ve had to deal with my own personal form of the author’s critic (I am not sure it isn’t an equivalent people! lol). I believe, the newest weak of the pure math argument is the fact it does not overlay Risk Studies and Maslow’s Need Steps near the top of the latest monetary math. Provided the true get back of your expenditures stays above your interest rate, you’re in the bucks. But shelter, eating, and you will liquid may be the highest root of the Need Hierarchy getting a reason. Based on your unique threats, it may not end up being best if you trust the capacity to liquidate investment for those who quickly become jobless, hospitalized, otherwise handicapped. For me, all of those requirements usually converge at a time. Youre prone to clean out your work through the a recession and stock-exchange is oftentimes maybe not carrying out one to really while in the such as a duration of. Then chances are you protected losses in principle together with incurring sufficient penalties and fees which will bring your real price out-of go back to at or even below your house rate of interest. Due to the fact let’s be honest, you are probably probably pull away from taxation deferred levels prior to old age age due to the fact those people were many successful to-be contributing huge amounts of money so you can to start with. You to combination is especially common for those who had the newest High Credit crunch in their working decades. I believe brand new author’s questionnaire a lot more than for issues that you might should fulfill when you realize early household payoff try very beneficial, since i wouldn’t actually ever suggest someone to attention thus intently towards that toes regarding economic balances that they forget all anybody else completely. Discover an extra one which I do want to create, but not. I really don’t need an excessive amount of engrossed, however, In my opinion you will see of numerous who will relate to they. Including conference the above mentioned requirements, are you presently worried you to an existing otherwise highly planning exists medical, hereditary, otherwise rational standing you will definitely flare-up right down to a keen additional produce and you will compromise that have a ceiling over your head to possess both yourself or your spouse(s)? You will find profoundly personal risks from inside the answer to you to definitely matter which can, plus in many circumstances undoubtedly is to, override an opportunity price of paying compared to protecting a coverage. As well as a subset of us, you to address will be the difference between impression safe enough in order to search let/get-off a posture otherwise enabling the brand new issues so you’re able to elevate and you will end you. Almost any your decision, your choice holds true.